The Home-Based Chronic Disease Management Inflection: A Hidden Catalyst Reshaping Health Futures

Emerging reimbursement and care delivery models signal a fundamental shift from episodic, clinic-centric healthcare toward integrated, home-based chronic disease management. This weak signal could recalibrate capital flows, compel regulatory evolution, and redefine healthcare industrial structures over the next decade.

As chronic diseases increasingly dominate health burdens globally, new policy enablers tied to digital health technologies and outcome-based reimbursements are quietly enabling rural and remote care transformation. The widespread but underappreciated emergence of programs incentivizing wearable devices and remote patient monitoring (RPM) within Medicaid/Medicare frameworks points to potentially profound systemic shifts. Recognizing this inflection is crucial to anticipate future health ecosystems beyond telehealth hype and superficial digital trends.

Signal Identification

This development qualifies as an emerging inflection indicator rather than a conventional trend or transient fad. Unlike typical telehealth expansions focused on access amplification, it signals structural recalibration by embedding chronic disease management into patients’ daily environments via reimbursed wearable and app-based monitoring. The Michigan Rural Health Transformation (RHT) program exemplifies operationalization beyond urban pilot projects, confirming a shift in care delivery expectations.

The time horizon is medium-term (5–10 years) with a high plausibility given ongoing Centers for Medicare & Medicaid Services (CMS) reimbursement adaptations and demographic trajectories. Primary sectors impacted include healthcare providers, medical device manufacturers, payers, regulatory bodies, and digital health innovators.

What Is Changing

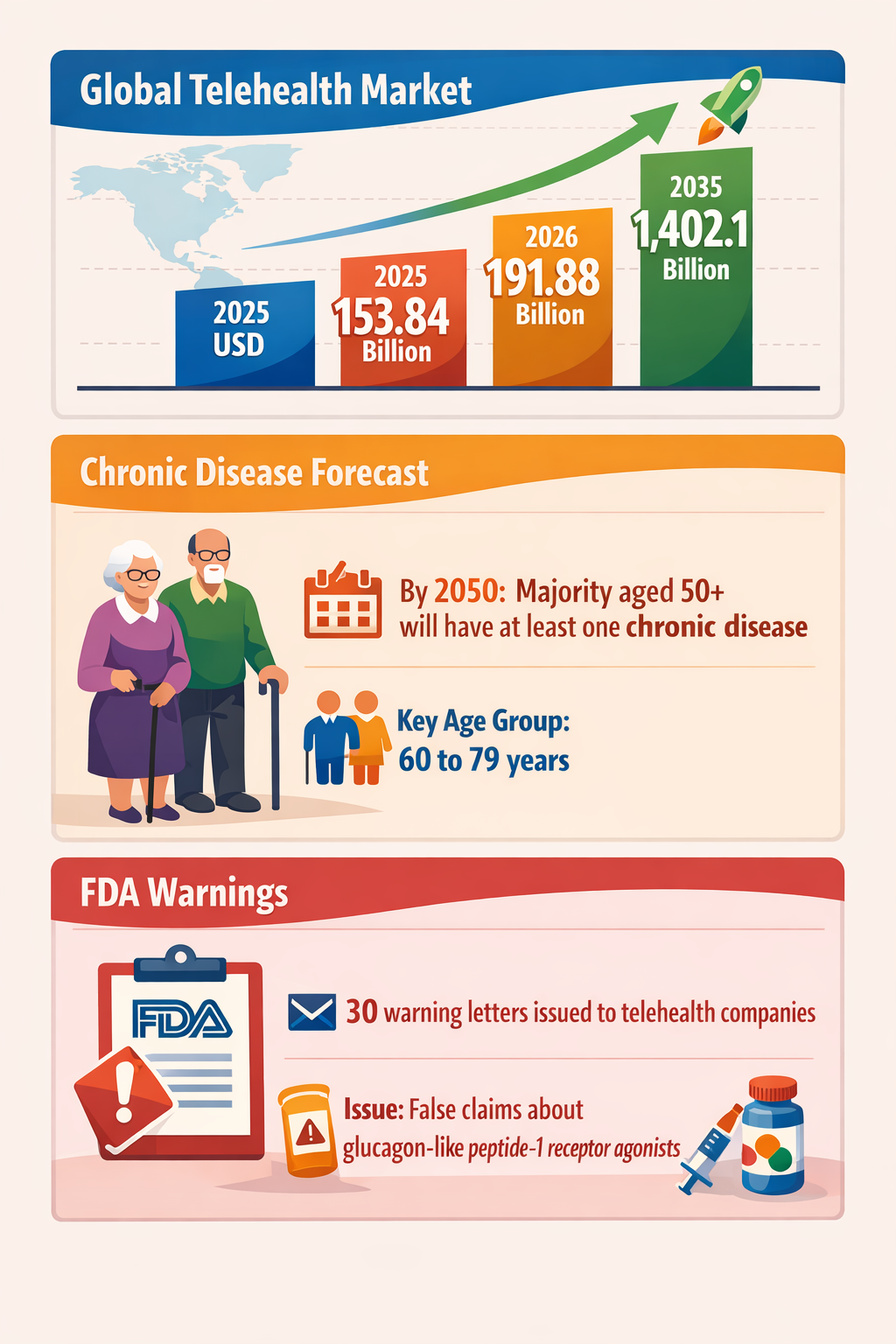

First, demographics are intensifying chronic disease pressure, with projections that a majority of adults over 50 will suffer at least one chronic illness by 2050 (>50 years cohort to >60–79 leading prevalence) (PMC 29/11/2022). This shift strains traditional episodic, facility-centered models ill-equipped for persistent condition management.

Simultaneously, CMS’s decision to reimburse wearables and apps in chronic disease monitoring based on demonstrable health outcomes marks a significant regulatory realignment. The linkage of coverage to outcomes data is noteworthy, moving incentives away from volume toward efficacy (Forbes 16/06/2026). This reframes digital health tools from ancillary conveniences to reimbursable medical interventions.

Meanwhile, Michigan’s Rural Health Transformation program operationalizes this paradigm by integrating remote patient monitoring into rural care delivery workflows, crucially extending care "beyond clinic walls" (Prevounce Blog 03/05/2026). This actual deployment highlights scalability potential in populations historically underserved by urban-centric health infrastructure.

Underlying these regulatory and programmatic signals, enforcement actions by the Food and Drug Administration (FDA) against telehealth companies misrepresenting compounded glucagon-like peptide-1 (GLP-1) receptor agonists further emphasize the maturation from unregulated telehealth novelty to more scrutinized remote care ecosystems (Prime Therapeutics 15/03/2026). This enforcement supports robust, evidence-based digital interventions underpinning broader reimbursement and delivery reforms.

Disruption Pathway

The recalibration starts with demonstrable chronic disease management efficacy from wearable-enabled remote monitoring, incentivized through CMS coverage conditioned on health outcomes. As providers accrue data validating clinical benefits and cost reductions, payer confidence grows, stimulating further reimbursement expansion.

Concurrently, rural programs like Michigan’s RHT serve as testbeds for integration, proving that decentralized care modalities reduce hospital admissions and improve patient quality of life. Success in these geographies addresses persistent care access gaps, fostering political and community buy-in for broader adoption.

Heightened FDA oversight of misleading claims assures a regulatory environment focused on credible, clinically validated digital therapeutics and diagnostics. This regulatory rigor incentivizes compliance and reduces reputational risks, facilitating capital flows toward compliant digital health innovators while discouraging opportunistic market entrants.

Structural stresses emerge as traditional healthcare revenue models reliant on episodic treatment erode, triggering provider business model transformations and reallocation of capital toward integrated care platforms. Providers, payers, and manufacturers must adapt to continuous data inflows and outcome-based contracts, requiring investment in data analytics, patient engagement, and interoperability standards.

Market feedback loops then accelerate ecosystem maturation; improved patient outcomes can translate to reduced downstream costs, encouraging payers and governments to upscale reimbursement programs. As deployment scales, industrial structures may shift—with digital health platforms becoming core assets within otherwise conventional hospital or insurance enterprises—blurring historic sector boundaries.

Dominant issuer-provider-payer governance arrangements could give way to hybrid, platform-centric governance models emphasizing data stewardship, patient empowerment, and outcome transparency, reshaping regulatory oversight frameworks accordingly.

Why This Matters

Strategic decisions today on capital allocation and regulatory frameworks are at a potential inflection point. Investors allocating toward digital health should consider wearables and RPM technology firms capable of delivering measurable chronic disease outcomes.

Regulators will need to balance evidence-based enforcement with adaptive reimbursement models that scale without undermining patient safety or inflating costs. Early investment in interoperability and outcome tracking infrastructure may confer competitive advantages.

Providers must reevaluate strategic positioning in light of shifting care delivery paradigms from episodic clinic visits to continuous home-based engagement. Legacy service models risk obsolescence unless integrated with digital monitoring and remote intervention capabilities.

Supply chains for medical devices and pharmaceuticals may see reorientation as demand patterns shift toward consumer-friendly, wearable, or home-use devices. Risk governance frameworks will increasingly incorporate digital therapeutics’ liability issues and data security considerations.

Implications

This development likely to result in structural change rather than short-term market noise, as demographic imperatives intersect with progressive reimbursement and care delivery reform.

It could compel entrenched healthcare incumbents to pursue digital platform integration or risk competitive erosion by more agile entrants focused on remote chronic care management.

However, this signal should not be confused with earlier telehealth hype cycles dependent solely on access expansion. The distinctive outcome-linked reimbursement and rural care integration differentiate it qualitatively.

Competing interpretations might argue that heterogeneous payer systems or technological fragmentation could slow scaling, but successful pilots and regulatory evolutions suggest growing systemic alignment.

Early Indicators to Monitor

- Expanded CMS reimbursement announcements clarifying outcome measurement criteria for wearables and apps

- Increased venture capital and corporate investment in RPM platforms demonstrating clinical impact in chronic disease

- Emergence of internationally harmonized interoperability standards for digital health data exchange

- Growing number of state-level rural health transformation initiatives beyond Michigan adopting remote disease management

- Public FDA enforcement actions targeting misleading telehealth and digital therapeutic claims

Disconfirming Signals

- Major CMS policy reversals or moratoriums on outcome-based reimbursement for wearables and digital disease management tools

- Widespread clinical studies failing to show sustained health improvements from remote monitoring in chronic disease cohorts

- Fragmentation of digital health data ecosystems leading to insurmountable interoperability barriers

- Significant backlash or adverse legal rulings against providers or tech firms over liability or data abuse in remote management

Strategic Questions

- How can capital deployment balance scale opportunities in RPM-enabled chronic disease management against interoperability and liability risks?

- What regulatory frameworks and outcome metrics will ensure credible yet scalable reimbursement models?

Keywords

Chronic Disease Management; Remote Patient Monitoring; Digital Health; Wearables; Healthcare Reimbursement; Rural Health; Regulatory Enforcement; Population Health

Bibliography

- The FDA issued 30 warning letters to telehealth companies for making false or misleading claims about compounded glucagon-like peptide-1 receptor agonists on their websites. Prime Therapeutics. Published 15/03/2026.

- The majority of the adult population 50 years and older, across all races, will have at least one chronic disease by 2050, with the majority between the ages of 60 to 79 years. PMC. Published 29/11/2022.

- CMS will reimburse device companies for wearables and apps used in chronic disease management, with full payment tied to improved health outcomes. Forbes. Published 16/06/2026.

- If implemented effectively, Michigan's RHT program could help rural providers extend care beyond clinic walls and bring more chronic disease management into patients' homes. Prevounce Blog. Published 03/05/2026.

- Demographic and epidemiological projections emphasize growing chronic disease burdens in aging populations. PMC. Published 29/11/2022.