Headline & Summary: The evidence around flying taxis and Advanced Air Mobility (AAM) reveals multiple accelerating signals pointing toward an imminent commercialization phase, driven by technological maturity, regulatory milestones, and strategic partnerships across global markets. Key momentum is seen in infrastructure development, regulatory progress particularly in FAA and UK CAA jurisdictions, and commercial deployments in pilot regions such as Dubai, Japan, and select US cities. At the same time, notable ecosystem convergence between eVTOL manufacturers, urban planners, and mobility platforms is shaping a multi-dimensional transformation driver with implications for urban transport, logistics, and airspace management. Challenges remain in certification, infrastructure roll-out, and public acceptance, but momentum is strong with tangible near-term inflection points expected by 2026-2028.

| Signal Name / Theme | Direction | Relative Frequency / % Change | Short Commentary |

|---|---|---|---|

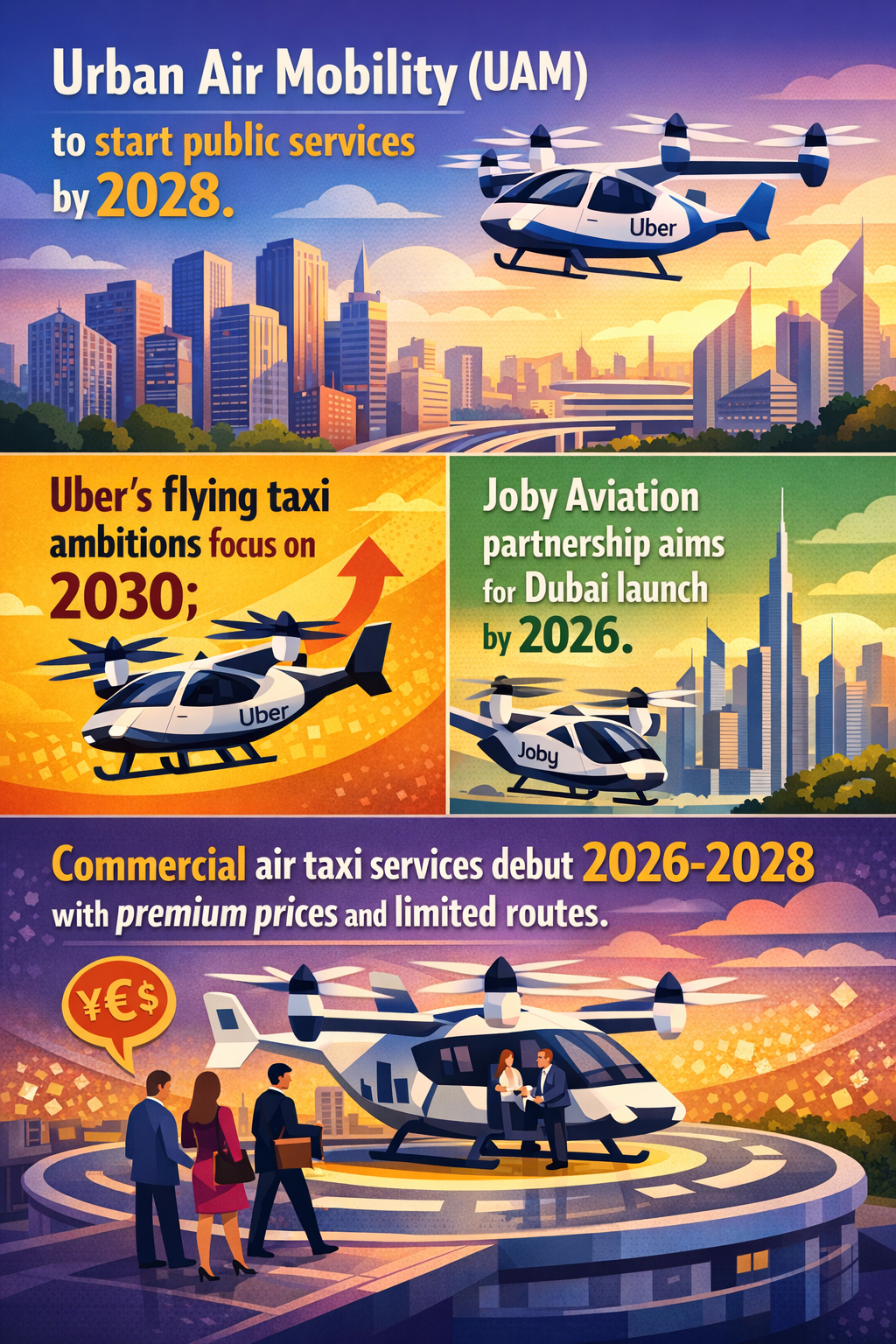

| Commercial Launch and Operational Expansion of eVTOL Flying Taxis | Accelerating | High — Multiple sources highlight 2026–2030 launch timelines, service expansion to multiple cities and countries | Commercial flying taxi services are edging closer with test flights, pilot programs, and infrastructure preparation underway globally, signaling a transition from demonstration to operation. Examples: Uber-Joby collaboration in Dubai (2026), Vertical Aerospace in Japan (pilot routes 2026), Waymo’s rapid robotaxi scaling also reflects mobility ecosystem growth. |

| Regulatory and Certification Progress for eVTOL and AAM | Accelerating | High — Intense recent activity on FAA, UK CAA, JCAB (Japan), and Chinese authorities with impending certifications and safety frameworks | Regulatory frameworks are maturing rapidly, with multiple jurisdictions progressing type certification pathways and setting safety standards. FAA certification expected within 1–2 years, UK’s CAA actively enabling future flights, and Japan advancing type validations. These regulatory moves were previously bottlenecks and now fuel accelerating market entry. |

| Strategic Industry Partnerships and Investment Growth | Accelerating | Significant funding growth — eVTOL funding exceeded $6.5B in 2025 from $40M in 2016; multiple pre-orders and JV announcements | Strong investor confidence and strategic partnerships (e.g., Uber-Joby, Vertical Aerospace-Marubeni, Harbinger-Phantom AI) underpin rapid ecosystem expansion, signaling consolidation and vertical integration trends. These moves boost operational readiness and global market reach. |

| Infrastructure Development: Vertiports and Airspace Management | Stable to Accelerating | Moderate frequency but increasing mentions of vertiport site selection, urban integration, and air traffic management initiatives | Growing focus on ground infrastructure (vertiports), charging stations, and airspace systems reflect convergent transformation, addressing the “chicken and egg” problem of ecosystem readiness. City-level planning (e.g., St. Pete, London) is emerging, but scale-up remains a pending challenge. |

| Public Perception, Noise, and Safety Concerns | Stable | Moderate — Consistently discussed with no accelerated shift, but still a key enabler/barrier | Concerns about noise, reliability, and pilot/operator trust remain present but steady. Advances in quieter eVTOL designs (55 dB noise levels) and incremental regulatory reassurance are helping manage risk and build tentative social license. |

Pattern Narrative:

The examined evidence depicts a rapidly maturing AAM ecosystem where the commercial operational phase is imminent, supported by tangible advancements across technology, regulation, funding, and infrastructure. The strong acceleration in certification efforts and strategic collaborations signals that the industry is moving beyond conceptual and pilot stages toward scalable service delivery. Concurrently, infrastructure — including vertiports and integrated urban airspace management — is emerging as a critical component to unlock mass adoption, although deployment scale and public acceptance remain ongoing challenges.

This momentum reflects a broader systemic convergence — aerospace engineering, urban planning, automotive OEM strategies, and digital infrastructure are increasingly integrated. The transformation driver here is the creation of new mobility networks combining ground and urban aerial transportation, potentially reshaping urban and regional travel patterns. Furthermore, the emerged archetypes — system integrators, service providers, hardware manufacturers, and ticket brokers — demonstrate that the industry is evolving towards a mature multi-stakeholder marketplace.

Implications:

Stakeholders should prioritize monitoring regulatory milestones and certification timelines closely, as these will be pivotal gatekeepers for market entry scale-up. Investment and partnership activities signal where consolidation and vertical integration might create competitive advantages or bottlenecks. Planning for vertiport and infrastructure deployment should accelerate, with supportive policies and community engagement to address potential public resistance. Urban and regional transport planners should begin scenario modeling for integrating AAM with existing modes. Lastly, continuous monitoring of safety, noise, and reliability outcomes from pilot programs will be critical to sustain public trust ahead of widescale deployments.